{kind=link}

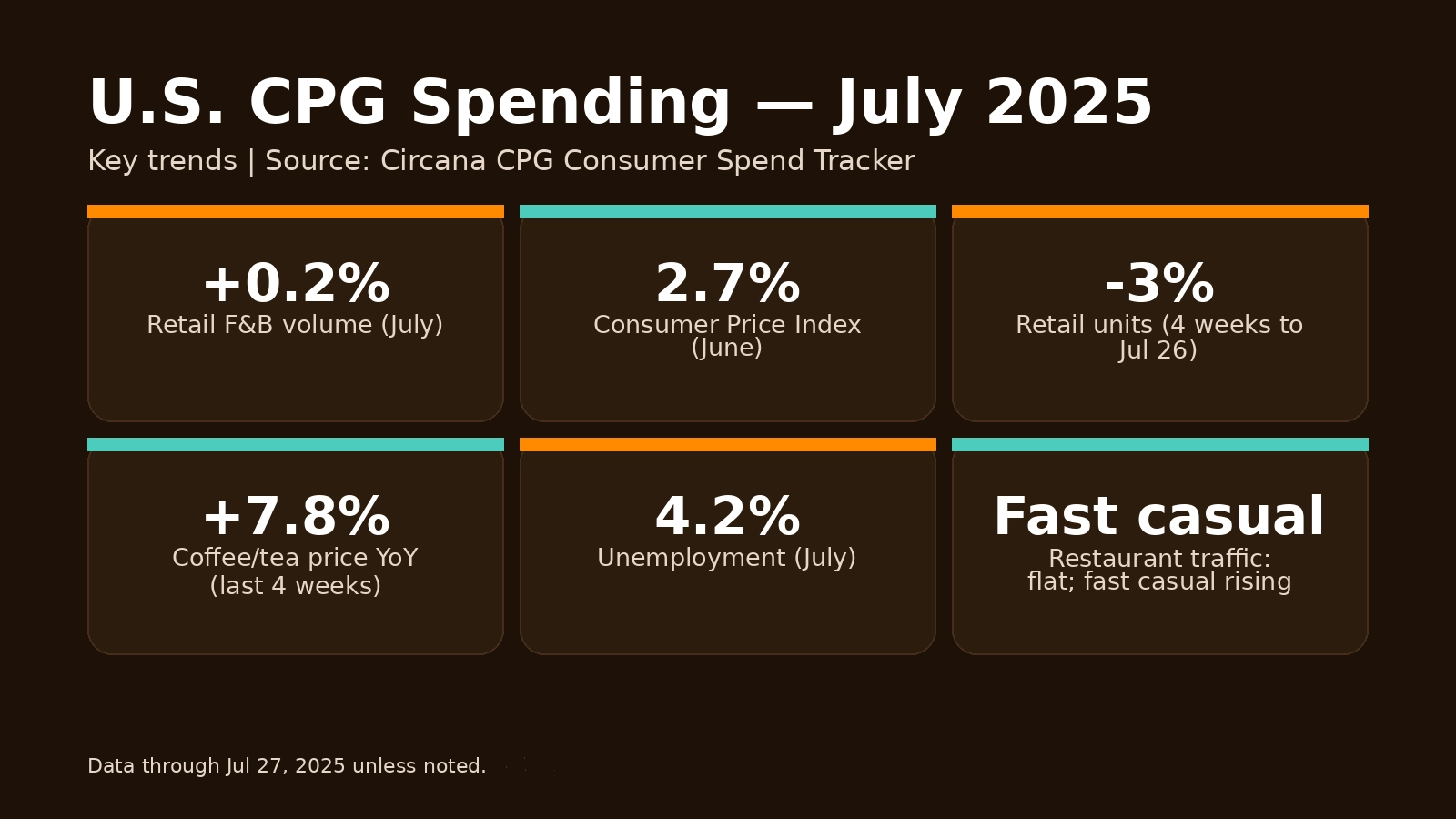

U.S. CPG spending continues to struggle under economic headwinds, even as July brought slight improvements in retail food and beverage (F&B) sales, according to Circana’s CPG Consumer Spend Tracker. Volume inched up 0.2% last month, reversing earlier declines but still falling short of historical norms. Dollar sales rose 3.2% year-to-date, driven mainly by price increases rather than stronger demand.

Consumers are focusing on nutrition-dense essentials such as meats, produce, and dairy while cutting back on snacks and sweets. This shift underscores a growing emphasis on affordability and health as households navigate tighter budgets.

Tariffs and Inflation Add Pressure

The Consumer Price Index climbed to 2.7% in June, signaling renewed inflationary pressure. Tariff-related costs are beginning to ripple through the economy after updated rates took effect on August 7. Most countries now face tariffs between 10% and 15%, while key trading partners see rates above 15%. These changes are expected to influence pricing across multiple consumer packaged goods categories, Circana reports.

Commodity volatility compounds the challenge. Coffee prices surged 7.8% year-over-year in July, up from 3.8% in the first quarter. Meat, cocoa, and nuts also saw price spikes, driven by supply constraints and premiumization trends.

Restaurants Flat, Fast Casual Gains Ground

While retail channels struggle, foodservice shows mixed results. Restaurant traffic remained flat in the latest four weeks, a notable improvement from the 2% decline over the past year. Fast casual operators lead the recovery, benefiting from weekday dine-in occasions and competitive chicken offerings.

Despite extended July promotions, retailers failed to spark significant demand. Sales for the four weeks ending July 26 were flat in dollars and down 3% in units, highlighting persistent consumer caution, according to Circana.

Related Article: Shoppers Choose Private Label Groceries as Food Costs Rise

Consumer Confidence Improves Slightly

Economic sentiment offers a glimmer of optimism. The University of Michigan Consumer Sentiment Index rose to 61.7 in July, up one point from June. However, confidence remains well below last year’s levels. The unemployment rate ticked up to 4.2%, while inflation expectations eased to 4.5%, suggesting consumers anticipate some relief but remain wary.

Non-Food CPG Faces Slowdown

Non-food CPG categories mirror the slowdown. Dollar sales grew 2.7% year-to-date, but unit sales slipped into negative territory. Price changes largely reflect channel and product mix shifts rather than shelf price hikes.

Home and kitchen products lead the decline as cost-conscious shoppers cut back on cleaning supplies and disposable goods. In contrast, beauty and personal care—especially fragrance and skincare—remain resilient, Circana’s data shows.

What’s Next for U.S. CPG Spending?

Industry analysts expect continued volatility through the second half of 2025. Tariffs, commodity costs, and shifting consumer priorities will shape pricing strategies and promotional activity. Retailers may lean on value-driven assortments and loyalty programs to maintain engagement, while foodservice operators capitalize on fast-casual momentum.

As economic uncertainty lingers, brands that balance affordability with quality stand the best chance of winning consumer trust.