{kind=link}

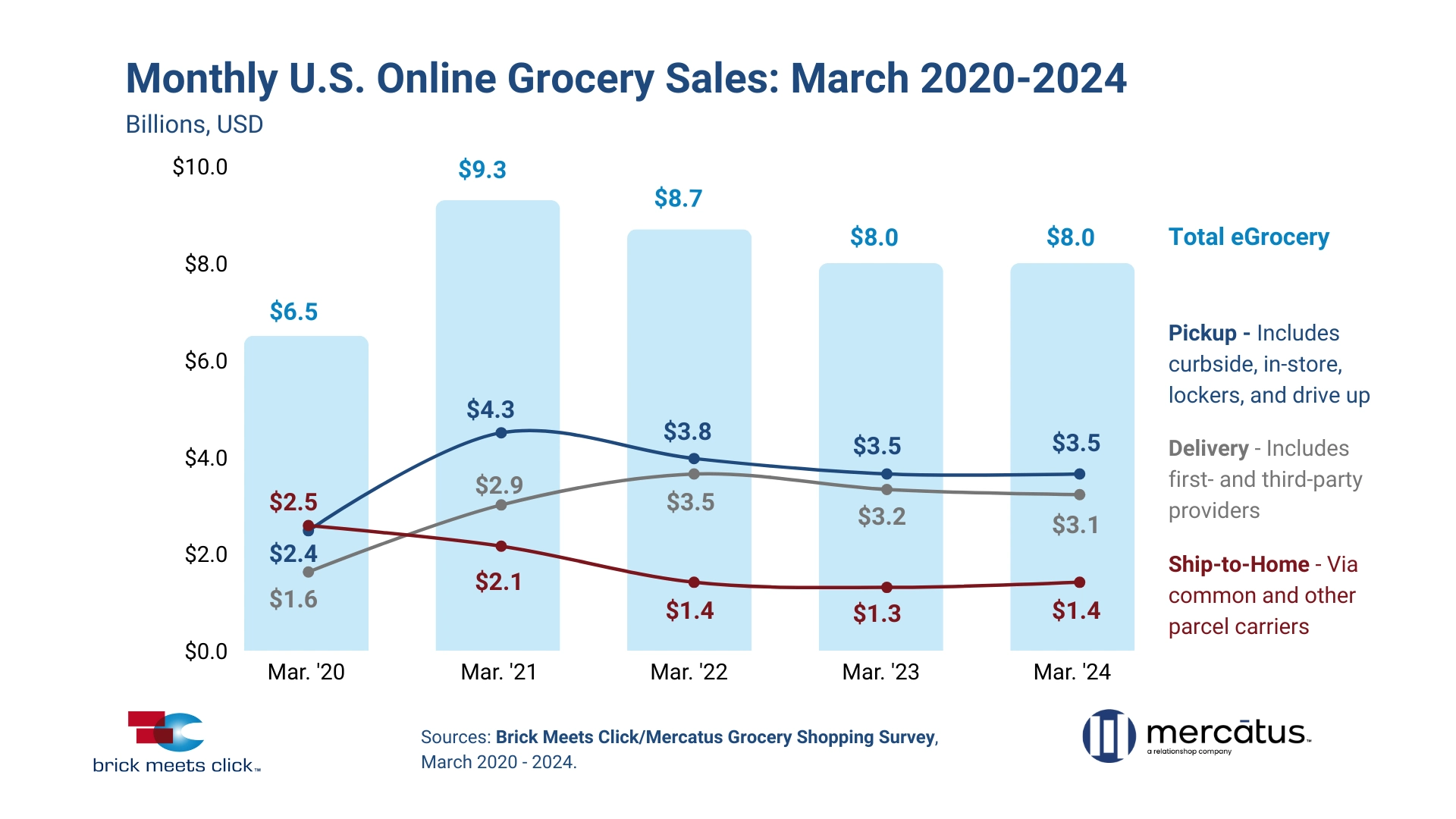

The overall U.S. online grocery market ended March with total monthly sales of $8.0 billion, holding steady compared to a year ago, according to the most recent Brick Meets Click/Mercatus Grocery Shopper Survey fielded March 29-30, 2024.

These monthly results are an improvement over March 2023, when total monthly eGrocery sales had fallen 8% yearly. Current sales are 23% above the levels posted in March 2020, the initial month of the pandemic in the U.S.

“While most people recognized that the pandemic was a catalyst for buying groceries online, few could fully anticipate the implications of that surge,” said David Bishop, partner at Brick Meets Click. “Now, four years after COVID-19 first impacted our everyday lives, eGrocery in the U.S. looks very different from both a contribution and growth perspective, and this will impact how grocers and others expand and drive profitability in their respective businesses moving forward.”

From a contribution perspective, the Pickup and Delivery share has grown at the expense of Ship-to-Home. Pickup, which accounted for less than one-third of eGrocery sales in 2019, quickly moved to the top spot when the pandemic started, and it has stayed there ever since, expanding 586 basis points (bps) from March 2020 to 43.2% this year.

Delivery, which represented one-quarter of all online sales in 2019, experienced an even more significant jump in market share, expanding by 1,488 bps during the same period to end March 2024 with 39.1%.

The past four years of sales results show that total eGrocery sales for March peaked in 2021 and have declined or been flat year-over-year since then. Regarding the specific methods customers use to receive those online orders, Ship-to-Home crested in March 2020, Pickup crested in 2021, and Delivery did so in 2022.

Recently, Ship-to-Home posted a gain of 5.9% in sales in March 2024 versus last year, while Pickup’s sales were unchanged, and Delivery’s monthly sales dipped 2.6%.

Related Article: Why Retailers and CPGs Fail to Harness AI Potential

The ongoing research shows that the online grocery customer pool size has become more well-defined and that future growth will likely happen more gradually.

In March 2024, the total eGrocery customer pool (which consists of active and lapsed or infrequent users) expanded to include 78.6% of all U.S. households, up just 13 bps versus the prior year and slightly less than the 16 bps it grew in March 2023 versus 2022. In contrast, at the end of the first month of the pandemic in 2020, online grocery household penetration finished at 70.8%.

While the overall eGrocery Monthly Active User (MAU) base as a share of total households more than doubled at the start of COVID-19, finishing March 2020 at 57.5%, the share of MAUs has generally remained in the 50% range.

Preferred Methods for Receiving Online Grocery Orders

Another thing that hasn’t changed much in the last four years is that most U.S. households continue to have strong preferences for how they receive their online grocery orders.

The share of MAUs that used only one method during the past 30 days has climbed 340 bps to 71.7% from March 2020 to 2024. However, the method(s) that households use has shifted.

Since March 2020, the share of MAUs that used Pickup has expanded more than ten percentage points, finishing March 2024 at 54.8%, the share of MAUs that used Delivery rose over 12 points to 38.4%, and Ship-to-Home’s share of MAUs plunged almost 20 points.

Competition online for active customers has also gotten more intense for Supermarkets – especially from Walmart.

Cross-Shopping Competition Intensifies

Before COVID, only 15% of the customers who bought online from Grocery (which includes Supermarkets and Hard Discount) also completed an online grocery order from a Mass retailer during the same month.

For March 2024, that cross-shopping rate stands at nearly 27% as reduced purchasing power continues to motivate some households to change where they buy groceries.

The elevated rate of cross-shopping potentially affects customer expectations based on experiences elsewhere, like with Mass. This may explain why the likelihood of using the same Grocery or Mass service again within the next month in March 2024 was 18% below pre-COVID intent rates, and the gap between Grocery and Mass has widened.

“Helping customers build their basket of goods by using tactics like personalized offers or targeted deals is not just key to growing sales but also to improving the chances that they’ll return,” said Mark Fairhurst, Global Chief Growth Officer at Mercatus. “For today’s grocers, keeping your online customers engaged is more important than ever as growth is more likely derived from increased order frequency and/or spend per order.”

Another challenge for most brick-and-mortar grocers is building a mobile app that assists customers as they shop, whether online or in-store.

Mass retailers like Walmart and Target have already invested heavily in enhancing the perceived value of using their mobile apps, and it shows.

The latest research found that 76% of households that primarily buy groceries from Walmart and groceries online completed one or more eGrocery orders with Walmart during March 2024.

For households that primarily shop at a supermarket and buy groceries online, only 60% buy groceries online from a supermarket.