{kind=link}

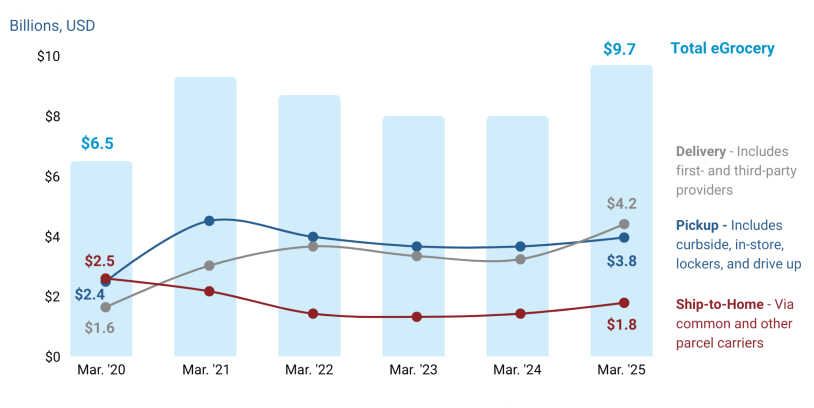

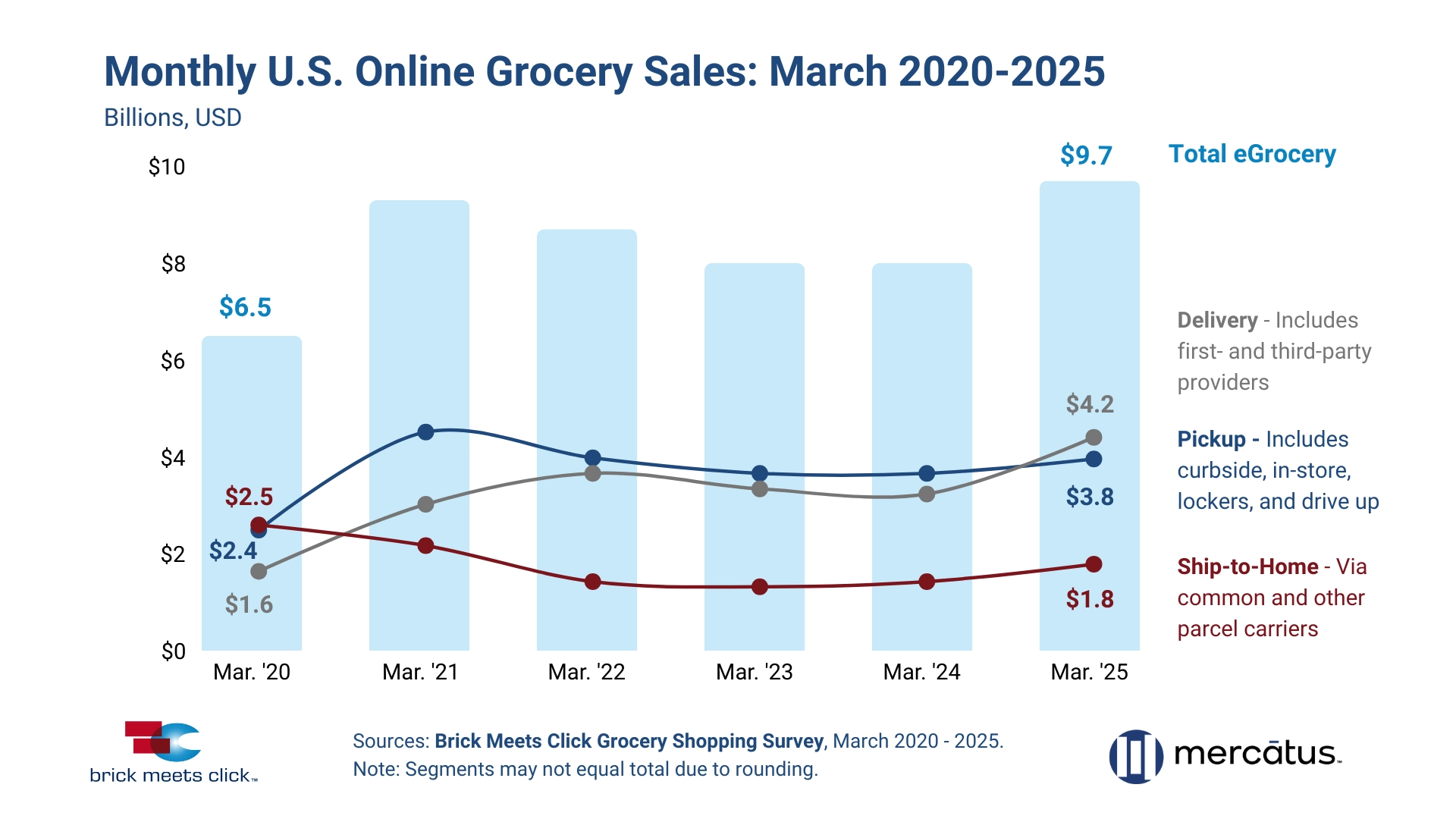

U.S. eGrocery sales climbed 21% year over year in March 2025, reaching $9.7 billion, according to Brick Meets Click’s latest survey. The monthly performance highlights a strong rebound in consumer demand, driven mainly by Delivery services and steep promotions on memberships and subscriptions.

Delivery continued to outpace other fulfillment methods, jumping more than 30% from March 2024. The rise followed a steady expansion of monthly active users (MAUs), signaling renewed consumer confidence and convenience-driven habits.

Pandemic-Era Trends Evolve into Sustained Growth

March marked five years since the COVID-19 pandemic transformed how Americans shop for groceries. Back in August 2019, eGrocery sales stood at just $2 billion. By March 2020, they skyrocketed to $6.5 billion as lockdowns forced households to adopt online shopping.

Although sales peaked in early 2021, the market has stabilized and resumed upward momentum. Since mid-2024, promotional strategies—including subscription discounts—have added another 20% to eGrocery growth. March 2025 became the eighth straight month of sales surpassing $9.5 billion.

Delivery Dominates eGrocery Sales

Consumer preference has shifted dramatically over the past five years. In 2019, Ship-to-Home accounted for 42% of eGrocery sales. Today, it trails significantly with only an 18% share. Delivery, by contrast, surged to 43%, up from 26% in 2019. Pickup now claims nearly 39% of the market.

“Delivery’s remarkable year-over-year rebound highlights the potency of promotional strategies that help customers save more money,” said David Bishop, partner at Brick Meets Click.

Retailers like Instacart, Shipt, and supermarket chains have all capitalized on this shift. With increased order frequency and higher average order values, memberships have become central to maintaining loyalty and recurring revenue.

More Consumers Use Multiple Fulfillment Methods

Before the pandemic, 85% of online grocery shoppers used only one fulfillment method per month. That figure dropped to 70% in March 2020 and has held steady since. On eGrocery sales, this shift shows that customers mix Pickup, Delivery, and Ship-to-Home options based on convenience, trip type, and price.

Each method attracts different types of customers. For instance, Ship-to-Home spiked in 2020 during lockdowns, then receded as in-store access resumed. Delivery flourished through 2022 but contracted under inflation pressures until promotions revived its appeal in 2024. Meanwhile, Pickup’s popularity dipped in 2021 but has rebounded in 2025 thanks to supermarket-driven incentives.

Related Article: The Omnichannel Shopper Blends Online and In-Store Buying for Convenience

eGrocery Sales Remain Strong

The percentage of U.S. households using online grocery services remains elevated. Pre-pandemic levels were under 25%. That figure jumped to 57% in March 2020 and has hovered between 57% and 61% through early 2025.

The monthly eGrocery order frequency has also risen—from 2.0 orders before COVID-19 to 2.6 as of March 2025. “Customer expectations around online grocery have only increased since COVID-19 pushed many to give it a try,” said Mark Fairhurst, chief growth marketing officer at Mercatus.

Retailers Must Adapt to Stay Competitive

With more options available and customer expectations higher than ever, grocers face a new set of challenges. Those who elevate the digital experience with relevant deals and personalized rewards stand to win market share.

eGrocery sales are no longer riding pandemic momentum—they’re being earned through innovative pricing strategies, flexible fulfillment options, and consistent consumer engagement. The path looks more competitive as retailers double down on loyalty and digital infrastructure.