{kind=link}

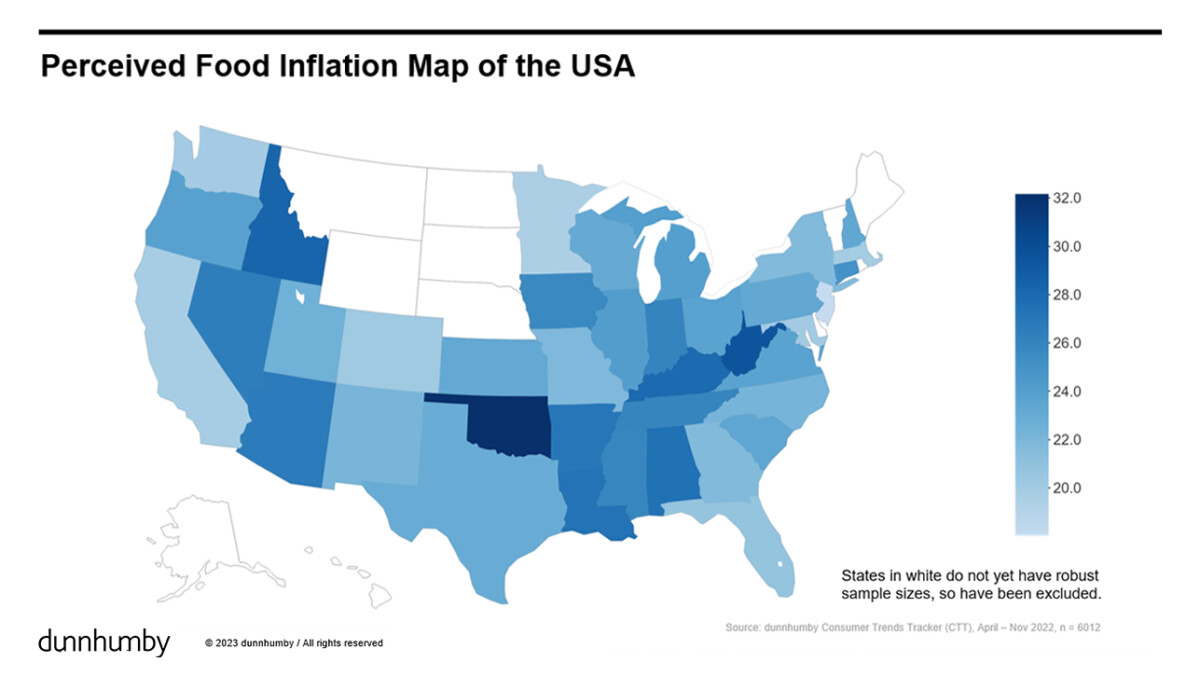

American consumers believe that grocery retailers are earning a 35.2% net profit margin, 14 times higher than grocers’ actual net profit margin average of 2.5% and that food-at-home inflation is 24.3%, double the annual rate reported by the U.S. Bureau of Labor Statistics.

Dunnhumby’s latest Consumer Trends Tracker (CTT) revealed a significant discrepancy between how consumers perceive inflation and grocery store profits and the actual figures.

The CTT is part of the dunnhumby Quarterly, a strategic market analysis of key retail themes, with the third edition focusing on navigating uncertainty.

Dunnhumby reported that in the third wave of the CTT, he also found that, although perceived inflation has reached a new high, customers are coping a little better compared to the last round of the survey. Consumers who reported having difficulty covering an unexpected expense of $400 dropped from 64% in July to 60% in November 2022. In addition, 48% of consumers reported they are getting the kind of food they want to eat compared to 43% in the second wave.

“In this latest wave of our CTT study, we found that retailers are in a precarious position with their brand perception since customers are vastly over-estimating grocers’ store profit margins and inflation rates while they themselves are battling food prices,” said Matt O’Grady, president of the Americas, dunnhumby. “Retailers need to show they are empathetic to customers through their prices, their rewards/loyalty offers, and with messaging to best support shoppers during these challenging financial times.”

Key findings from the study:

- Inflation worries are driving customer sentiment. When consumers were asked, as part of the survey, why customer sentiment is the lowest it has been in 50 years, consumers responded by a five to one margin that inflation was the cause, with covid coming in a distant second. When asked about 2023, only 22% of respondents predicted inflation and the country’s state would improve. Forty-seven percent of respondents predicted inflation and the state of the country would improve three years from now. Over a five-year period, 54% of consumers are optimistic that their own finances and the state of the country will improve.

- Younger shoppers are most optimistic, but only in the short term. For 2023, 31% of consumers aged 18-34 believe their finances and the state of the country will improve, compared to just 13% of consumers over 65. Over a three and five-year timeframe, there were no significant differences by age.

Related Article: Inflation and its Impact on Consumer Spending in 2023

- Food insecurity remains a problem. Thirty-one percent of households reported skipping or reducing the size of a meal for financial reasons. Thirty-nine percent of respondents under the age of 44 have skipped or reduced meal sizes. And households with children at home are 8% more likely than adult-only households to have skipped or reduced meal sizes. Consumers living in Idaho, Oklahoma, Arkansas, Tennessee, and West Virginia reported the highest numbers, where over 40% had skipped or reduced the size of a meal in the last year. Consumers living in Washington, Minnesota, Michigan, Massachusetts, and Maryland reported the lowest numbers, with approximately 20% having skipped or reduced the size of a meal in the last year.

- While improving slightly, most consumers continue to struggle financially. No state is immune, but the states with the highest rate of financial insecurity (75%) are Oregon, Oklahoma, Louisiana, and West Virginia. The states with the lowest rates of financial insecurity (45%) are Minnesota, Wisconsin, Maryland, and Delaware.

- Consumers want easy-to-shop and more convenient eCommerce solutions. Eighty-one percent (up 4%) of consumers say easy-to-shop websites and apps are important to them, and 78% (up 4%) want retailers to have more convenient delivery and pick-up time slots. For consumers aged 55 and over, ease and convenience are even more important. In this age group, 84% say easy-to-shop websites and apps are important to them, and 81% want convenient delivery/pick-up time slots available. Families are 16% more likely to interact with a store’s app and have a 10% greater need for the retailer to pick products as well as they would, compared to shoppers without children.

- Consumers want retailers to help them make healthy choices. Forty-four percent of consumers reported it was very or extremely important for retailers to help them make healthy choices, an increase of 3% from the previous wave. In addition, 48% reported they choose healthy foods while shopping (up 2%), 40% read diet and nutrition information (up 2%), and 29% buy products for a specific diet when they shop. The top five diets in the U.S. cited in the survey are 1) Keto; 2) Low carb; 3) Low sugar; 4) Vegetarian; 5) Gluten free.