{kind=link}

U.S. convenience stores experienced a 16th straight year of record in-store sales in 2018, according to newly released National Association of Convenience Stores (NACS) State of the Industry data. Foodservice sales continue to be a key focus area for the convenience store channel.

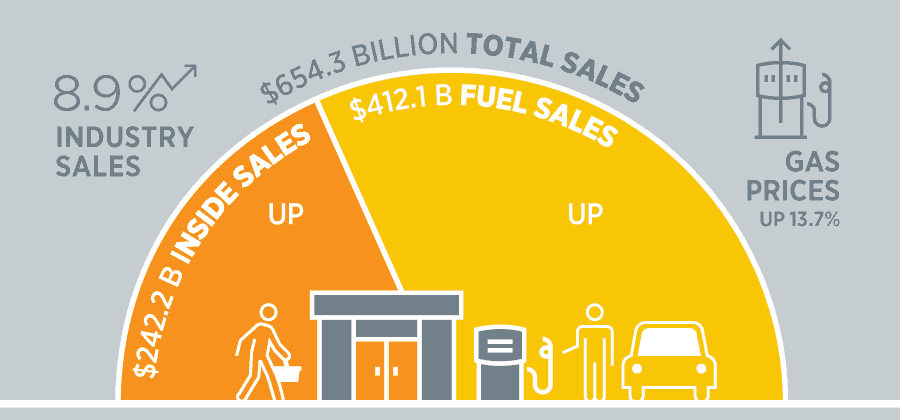

U.S. convenience stores sales overall surged 8.9% to $654.3 billion, led by a 13.2% increase in fuel sales, which account for 69.6% of total sales. In-store sales increased 2.2% to a record $242.2 billion. Overall, convenience stores sales are 3.1% of the U.S. gross domestic product of $20.5 trillion.

Higher gas prices, up 13.7% from $2.37 per gallon in 2017 to $2.69 per gallon in 2018, contributed to the increase in overall industry sales. Fuel margins, which have increased over the last five years, were also higher in 2018, up 7.5% to 23.35 cents per gallon, while gallons sold decreased by 0.4%.

“Fuel sales were strong in 2018 but consumers were making fewer stops to refuel, which suggests that greater fuel efficiency in vehicles is translating to less trips per week to the convenience store,” said Andy Jones, NACS vice chairman of research and president/CEO of Sprint Food Stores Inc. in Augusta, Georgia. “Utilizing NACS research can help retailers track trips per transaction and develop new marketing strategies to bring customers from the pump inside the store.”

Foodservice Powers In-Store Growth and Strategies

Foodservice sales accounted for 22.6% of in-store sales, a category that continues to be a key focus area for the convenience store channel. Foodservice is a broad category that mostly encompasses prepared food (69% of both category sales and profits) as well as commissary foods and hot, cold and frozen dispensed beverages.

The growth in foodservice also has led to an increase in store size. Overall, the average convenience store is 3,230 square feet. But as newer stores feature touchscreen food-ordering kiosks, add space for in-store seating and waiting areas and incorporate an open-kitchen design, the size of new stores has increased to 4,991 in rural locations, and 4,603 square feet in urban locations.

Cost of Growth in Convinience Stores

New business investments are also leading to higher direct store operating expenses (DSOE), which include wages, payroll taxes, health-care insurance, card fees—higher than overall industry pre-tax profit for the first time since 2014 ($11.1 billion vs. $11.0 billion)—utilities, repairs/maintenance and supplies, as well as several other categories including franchise fees and property taxes.

For the third consecutive year, DSOE has outpaced inside gross profit dollars, a trend that continues to create challenges for convenience retailers.

“The cost of growth, whether it’s higher acquisition multiples, new store construction or retrofitting older sites, has never been higher in our industry,” said Jones.

For example, the average cost to build a new store has increased over the last five years from $5.6 million to $7 million. “These are business trends that convenience retailers should be prepared to address as they continue evolving and growing their businesses.”

Employment and Wages

Beyond sales, convenience stores are an important part of the economy. The industry employed 2.36 million people in 2018, a slight decrease from 2.38 million in 2017. Part of this decline can be attributed to the slight decrease in the U.S. convenience store industry store count reported in March 2019.

Despite a tight labor market, store associate turnover decreased from 121% in 2017 to 118% in 2018; however, retailers are also paying employees more: Wages were up 4.4% and the average wage for a store associate increased to $10.74 per hour.

Category Performance

Convenience stores are the destination of choice for the 165 million U.S. customers who frequent their favorite location each day, and 83% of the items bought at a convenience store are consumed within the first hour of purchase.

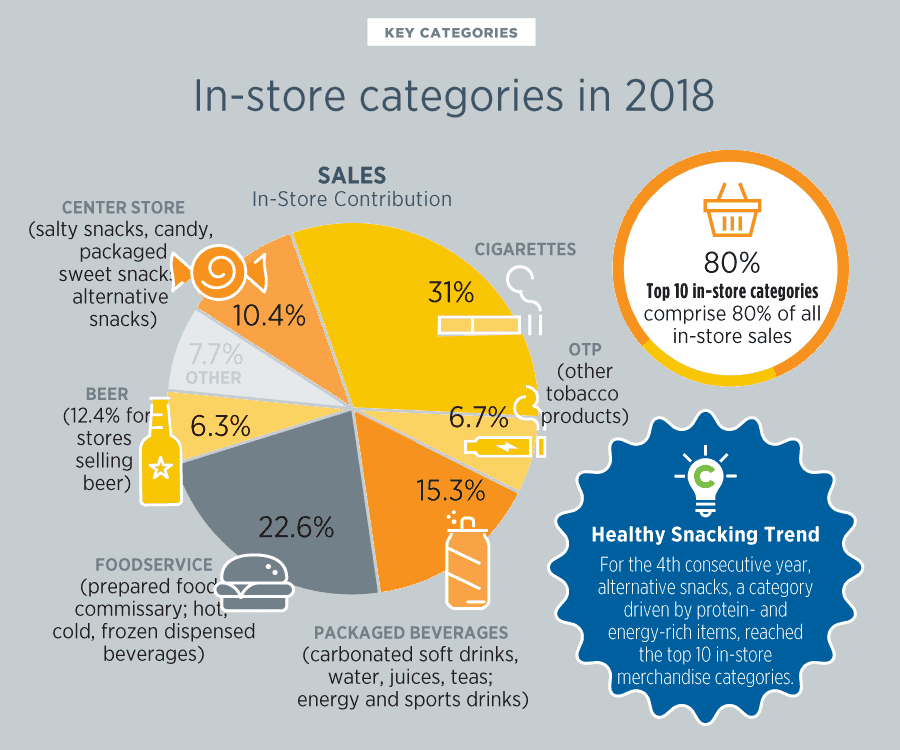

Here are overall merchandise sales groups as a percentage of overall merchandise sales:

- Cigarettes: 31% of in-store sales

- Foodservice (prepared and commissary food; hot, cold and dispensed beverages): 22.6%

- Packaged beverages (carbonated soft drinks, energy drinks, water, sports drinks, juices and teas): 15.3%

- Center of the store (salty, candy, packaged sweet snacks and alternative snacks): 10.4%

- Other tobacco products: 6.7%

- Beer: 6.3% (12.4% for stores selling beer)

- Other: 7.7%

Information provided by PRNewswire.